Category Archives for "General"

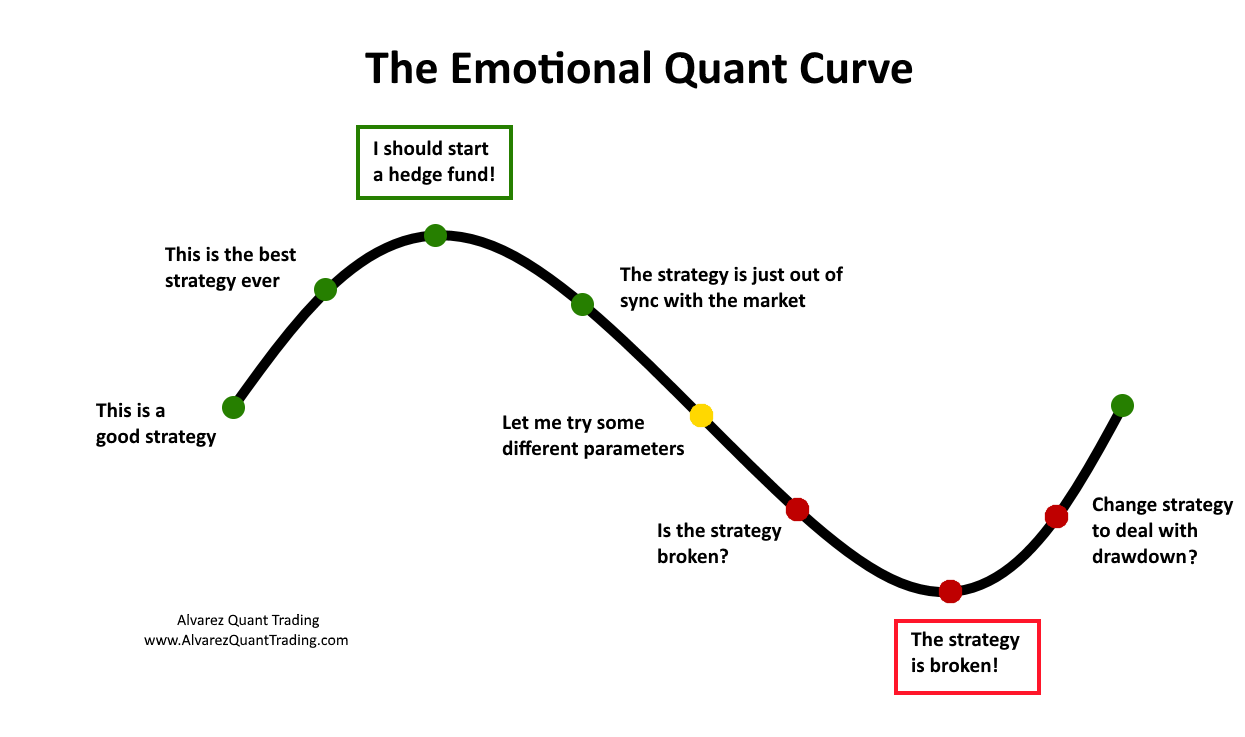

While writing my presentation for TradersFest 2018, I wanted to add the trader’s emotional curve. But looking at it closer, it did not capture my feelings as I go through the cycle of up and downs of trading a strategy. Here is my curve.

I have been on every part of this curve multiple times. October and November caused several strategies to go into the red part of the curve.

The top box of the curve, “I should start a hedge fund!” does not apply to me since I do not want to manage money. But lots of traders think about it and I chose that. For me, I would have changed it to “I can retire!”

Where are your strategies right now?

I will be giving a free online presentation, Getting started in Quantified Trading with a mean reversion strategy, at TradersFest 2018 on December 11, 2018. What to see my presentation?

Then sign up for TradersFest 2018.

It’s a FREE 2-day online event where you’ll learn trading strategies & techniques.

Topics from other presenters:

Topics that I will cover include:

If you want to join TradersFest, then click the link below and claim your spot (it’s free).

Here’s the link ==> Yes, Reserve My Spot!

See you at TradersFest!

The last few months, I have been busy doing research for Larry Connors’ new book, Buy The Fear, Sell The Greed. As always, it is fun and challenging to research for a book.

The book has seven strategies, trading both ETFs and stocks, with full rules and results. They are:

My favorite strategy is Crash because it is very similar to the short strategy I trade now. Those trades are hard to take. For each strategy there are good example trades and explanations of what the market was doing then.

Get the first chapter by clicking here.

The book is coming soon to Amazon.

I have written the difficulty in trading and testing short strategies. I had stopped trading my short strategy because it was too hard to trade psychologically for me. About nine months ago, I revisited my short strategy to see how it had been doing since I stopped and of course it has been doing just fine even during these very bullish times.

As strategy developers we often add rules to improve some metric, for example CAR or Sharpe Ratio. But just as important are rules that will help you keep trading the strategy even if the rule worsens your metrics. That is the case of what I did with my short strategy. I added two new rules that made the results worse, but I believe will make it easier for me to trade in the future.

You should have a plan for when you screw things up because I can guarantee it will happen. This is the screw up I did last night and how I handled it this morning. Enjoy this unplanned post.

Each night for 250 days of the year, I do the following for my trading.

Step 1: In the early evening, log into InteractiveBrokers, get the executions for the day, update my current positions and P&L spreadsheet. This is all done with a push of a couple of buttons. Last, push button in Excel that starts code that waits for data to be updated for the day and then runs my scans in AmiBroker and imports results into Excel. Time to do 2 minutes

This post is the continuation of the steps for creating a mean reversion strategy from the first part of The ABCs of creating a mean reversion strategy – Part 1. You can also listen to part 2 of my interview on Better System Trader here.

A quick recap of the topics covered in part 1. I covered trading universe, indicators to measure daily mean reversion, combining multiple mean reversion indicators, and last bar mean reversion.

I was recently interviewed on Better System Trader, click here for part one of the interview, about the steps for creating a stock mean reversion strategy. I will be covering and expanding on the topics from the interview. These steps, for the most part, would apply to any strategy one is creating. The focus will be a long stock mean reversion strategy using daily bars.

Like all traders, I am always on the lookout for any new indicators better than the ones I am using. I have been using and promoting RSI2 since 2004 for mean reversion trading. I created the ConnorsRSI in 2012. Am I married to these indicators? No. If I find something ‘better’ I will drop them. I came across this article Battle of the oscillators, I had to try it out.

One thing to understand, is that each situation is different. An indicator that works great on ETFs may work not as well on futures. Also, each person has a different metric on what is ‘better.’

I am frequently asked if I do out-of-sample testing. The short answer is not always and when I do, it is not how most people do the test. There are lots of considerations and pitfalls to avoid when doing out-of-sample testing. Out-of-sample testing is not the panacea it is made out to be. There are lots of grey areas which I will discuss below.

While doing the research for the next article based on Simple ConnorsRSI Strategy on S&P500 Stocks, I discovered that I had not tested what I wanted. Unfortunately errors are made while doing research and my goal is to catch them before publishing them. I did not in this case. Fortunately the results did not significantly change. The top CAR went from 27.32 to 26.63. As usual the error made the numbers comes down. Why is it that it never happens that they go up? See the post for the corrected numbers. I have also uploaded a new corrected spreadsheet.

Good Quant Trading,