Category Archives for "Mean Reversion"

While playing around with a 2 period RSI (Relative Strength Index) mean reversion strategy, I came up with a very simple rule change with a much larger impact on the results than expected. I doubled the compounded annual growth rate and cut the maximum drawdown in half. That never happens.

In my optimization runs the best CAR went from lows 10’s to the low 20’s with this rule change.

One of the first tests I did when I got AmiBroker twenty years ago was a mean reversion test. It was a classic set up, a stock in an uptrend, followed by a pullback. But the entry differed from what I do now. The entry waited for a confirmation of the trend back up. The trade would enter when the stock crossed above the previous day’s high. The exit was also different. The exit was on a close below the lowest low of the last (2,5) days. The results were not very good, so I gave up on it. I did not do test entering on the open or on further intraday pullback or exiting on the bounce. If I had, I would have started my mean reversion trading several years earlier, which would have added several more years of large edges trading. Oh well, I was just a beginner researcher then.

Recently I got curious about waiting for confirmation before entering a trade. Now that I know more about entries and exits, would it give good results. How would these results compare to waiting for further intraday pullback or entering at the open? Time to discover.

I have written the difficulty in trading and testing short strategies. I had stopped trading my short strategy because it was too hard to trade psychologically for me. About nine months ago, I revisited my short strategy to see how it had been doing since I stopped and of course it has been doing just fine even during these very bullish times.

As strategy developers we often add rules to improve some metric, for example CAR or Sharpe Ratio. But just as important are rules that will help you keep trading the strategy even if the rule worsens your metrics. That is the case of what I did with my short strategy. I added two new rules that made the results worse, but I believe will make it easier for me to trade in the future.

A mean reversion strategy I trade was developed with another researcher. This strategy enters on a further intraday weakness with a limit order and typically exits a few days later when the stock bounces. Recently this researcher sent me and email saying “Try the strategy as a day trade. Enter at the open and exit at the close. Surprisingly good results.”

A reader emailed me about testing a weekly mean reversion rotation strategy on S&P500 stocks. My first thought was, why had I not done this type of test before? The very first strategy that I worked on with Larry Connors was this type of strategy. The strategy I will be testing today is a simpler version and different universe but how well will it hold up?

Testing period is from 1/1/2007 to 10/31/2017.

Setup

Each weekend, take all the stocks that have setup and then rank using one of the mean reversion methods below. Buy top 5 that are most sold off. Hold 1 week and sell. Then buy the ones that are now the most sold off

This post is the continuation of the steps for creating a mean reversion strategy from the first part of The ABCs of creating a mean reversion strategy – Part 1. You can also listen to part 2 of my interview on Better System Trader here.

A quick recap of the topics covered in part 1. I covered trading universe, indicators to measure daily mean reversion, combining multiple mean reversion indicators, and last bar mean reversion.

I was recently interviewed on Better System Trader, click here for part one of the interview, about the steps for creating a stock mean reversion strategy. I will be covering and expanding on the topics from the interview. These steps, for the most part, would apply to any strategy one is creating. The focus will be a long stock mean reversion strategy using daily bars.

Like all traders, I am always on the lookout for any new indicators better than the ones I am using. I have been using and promoting RSI2 since 2004 for mean reversion trading. I created the ConnorsRSI in 2012. Am I married to these indicators? No. If I find something ‘better’ I will drop them. I came across this article Battle of the oscillators, I had to try it out.

One thing to understand, is that each situation is different. An indicator that works great on ETFs may work not as well on futures. Also, each person has a different metric on what is ‘better.’

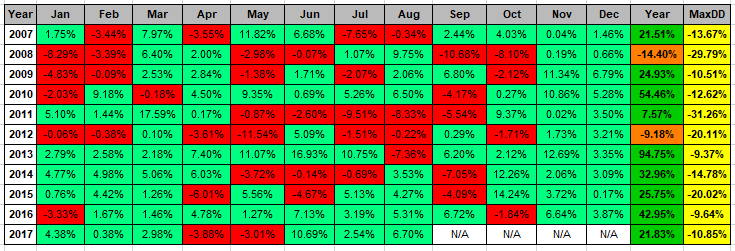

I recently had someone email me about the performance of a strategy I created back in late 2005/early 2006 and traded for a few years. I remember the strategy being a daily mean reversion set up with an intraday pullback entry. I figured it probably had not done well over the last decade. I stopped trading in the middle of 2008 because I did not like how it was behaving. In the backtest it did well in bear markets but was not doing so in the middle of 2008.

I ran the strategy from 2007, using the rules as they were published and was pleasantly surprised by the results. A CAR of 25%. Overall not too bad. Wish I had still been trading it. This is an eleven year out of sample test.

In the previous post, Simple ConnorsRSI Strategy on S&P500 Stocks, I showed a simple strategy which I optimized which gave 1,300 variations. Today, I will cover various methods to choose a strategy to potentially trade.