- in General by Cesar Alvarez

Bad Month for Your Strategy? Should You Change It?

A strategy you have been trading for years has just had a terrible month. Looking at the market environment, you think these trades should not have been taken. You make some “small” changes to your strategy and now the backtest shows that the terrible month is OK and the overall strategy statistics improve. Should you keep that change in your strategy?

For the longest time, I would keep that change. But it felt like overfitting. Then I thought, this is making the strategy better so I should keep it. This issue came up recently from a strategy that just had its worst drawdown. How do I handle this situation now?

First, I acknowledge that I am reacting to the market. These changes are being driven by emotions that come with losing money. This will become important later. We never seem to make changes when we have a huge winning month.

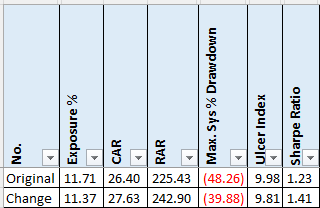

Next, I code up the changes that “improve” the strategy. To evaluate the changes, I look at metrics I care about which are CAR, drawdowns and yearly returns. Here we have high-level metrics.

Have the changes had a meaningful impact on these metrics? If not, then I should follow my rule of not adding rules unless the rules really helps. Here, we can see 5% increase in CAR, which is small and mostly meaningless. But MDD drops 17% drop which is great to see. I don’t use Sharpe but I know it is popular. We see a 15% increase in Sharpe, which is also good. So far that change looks good.

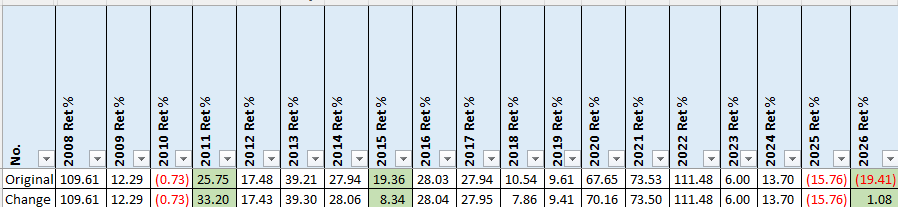

Now let’s look at yearly returns.

First, we can see that most years have no change. There are three years with big changes. The biggest change is 2026 as we would expect because I am trying to ‘fix’ that. These changes feel like curve fitting because of how few changes there are on the yearly returns.

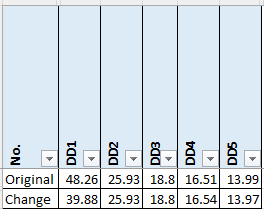

Looking at the top five drawdowns.

Here we see that the change only fixed the worst drawdown. This is not a good sign. Had the other drawdowns also become better, I would be more inclined to keep the change.

So far, this is looking like curve fitting to the recent market events.

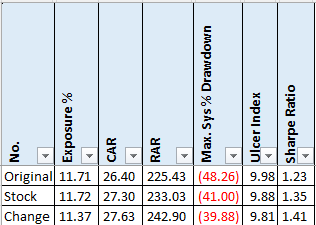

Next, I go back to the original rules and add specific code that avoids the trades that caused me to reevaluate the strategy. For example, do not trade a trade in XYZ or ABC in April of 2026. This allows me to see how much of the improvement I am seeing is coming simply from not taking these trades.

Here we can see that avoiding these two trades produced most of the improvement.

Now, it feels like curve fitting to the recent market and I would not make the changes.

But if the changes pass all the above, now comes the hard part. I put these changes on hold for two to three months. It is not likely that the market conditions that caused me to reevaluate the strategy will happen during this time. But that time gives me time to distance myself from the emotions of losing money.

Several months later, I revisit my changes and the improvements. What I have found is that usually I realize I was reacting to the moment and trying to justify the changes. In that case, I continue with the original strategy. Though sometimes, it feels right and I make the change. But now I feel better about the change.

Be careful when changing a strategy because of recent market action.

Backtesting platform used: AmiBroker. Data provider: Norgate Data (referral link)

Good quant trading,