Category Archives for "ETFs"

A research friend recently sent me a link to The #1 Stock In The World. Besides being a blatant title to get one’s attention (and it worked on me), I found the idea interesting along with my research friends. I have been trying to add either XIV or VXX to my trading in some small way. The article is only doing a buy and hold on XIV but it peaked my interest to try some other ideas.

The post ETF Sector Rotation generated good ideas on what to try differently. This post will research two ideas using Fidelity sector mutual funds. The previous post focused on two ideas on the Select Sector SPDR ETFs.

The post ETF Sector Rotation generated some good ideas on what to try differently. This post will focus on two ideas on the Select Sector SPDR ETFs. The next post will look at two ideas using Fidelity sector mutual funds.

A popular topic lately has been “Smart beta” ETFs. What is smart beta? It is using different ways to weight an index and the ETF that tracks it. For example, the S&P500 index is a capitalization weighted index. Bigger companies have a larger portion of the index. If you look at the SPY, Apple which is the largest company, accounts for 4% of the index (https://www.spdrs.com/product/fund.seam?ticker=spy). Other ways one can weight an index are equal weight, by volatility, by fundamental measures, by technical measures and so on. Why would you do this? To beat the returns of the S&P500 index . But are these other ways better?

David Weilmuenster is today’s guest author. David and I worked together at Connors Research for eight years and is one great researcher and AmiBroker programmer.

Brochures for professionally managed investments and academic white papers on long term investing almost always praise the benefits of regularly re-balancing a portfolio. The benefits can arise from the interaction, or correlation, of periodic returns among the constituent assets in a portfolio. As the correlations among constituent assets decrease, the long term returns of the overall portfolio generally will increase with regular re-balancing. This has become known as “the only free lunch in investing”, although it does not work out that way in all situations.

My recent research has been in ETFs which I have not explored in several years. ETF sector rotation has always intrigued me. The idea seems so simple that it should work. Always be in the sector that has been doing the best. I like simple but does it work? If not, can we make it work?

How should one develop a strategy for leveraged ETFs? Do you develop the strategy on the unleveraged ETF and then apply the rules to the leveraged ETF? Or do you develop the strategy on the leveraged ETF directly? Or do you develop the strategy on the unleveraged ETF then use signals on that to trade the leveraged ETF? On first blush one would think that all three methods would produce identical results. But as we know, the obvious is rarely the right thing for strategy development.

From my post on Heikin-Ashi Charts, another researcher wrote Luck: The Difference Between Hired or Fired about how luck of the draw could account for the difference in returns depending on the starting date. This is a completely valid question. Are three better returns for a strategy in a particular area of the month or is it random? I do believe that luck plays a large part in our trading results, which is a future blog post. But from previous work on 5 day holds, I know that the end of the month and beginning on the month tend to be better times for ETF mean reversion.

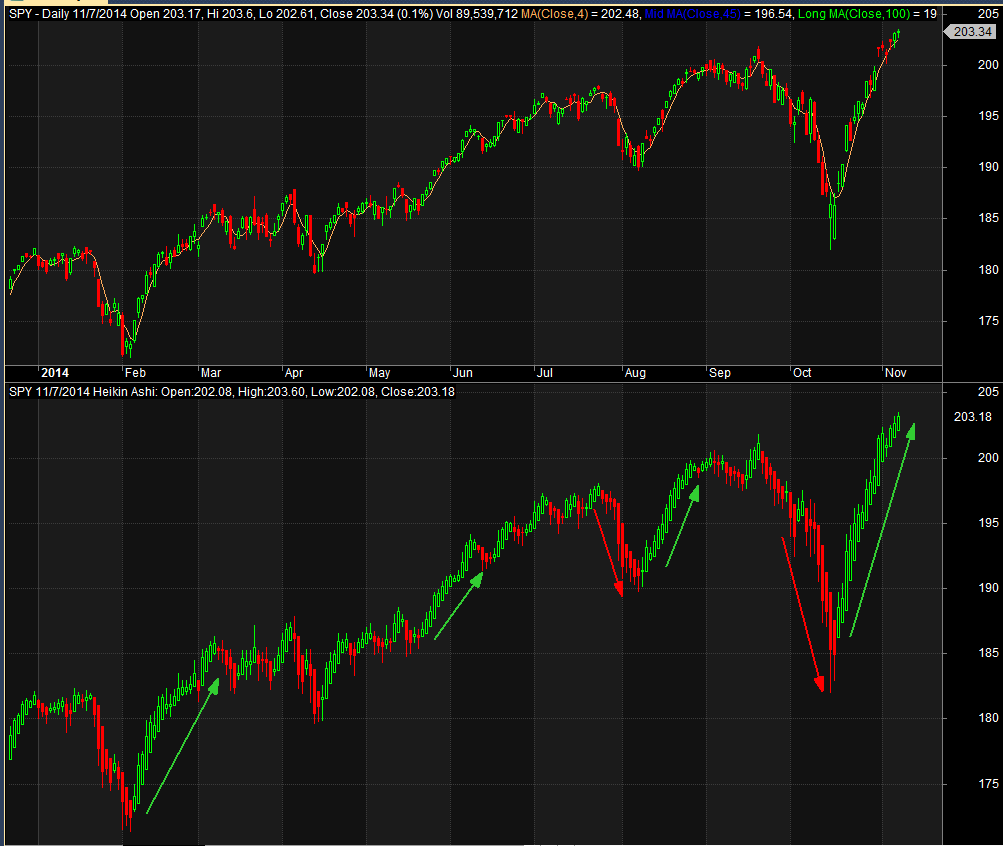

A reader recently introduced me to Heikin-Ashi charts. Popular with forex traders for showing trends which at first look of chart sure seems that way. Look at these two daily charts. The top one is a standard Candlestick chart while the bottom is Heikin-Ashi chart.

The trend of unbroken green sure seems more obvious and stronger in the Heikin-Ashi chart. Will testing confirm this?

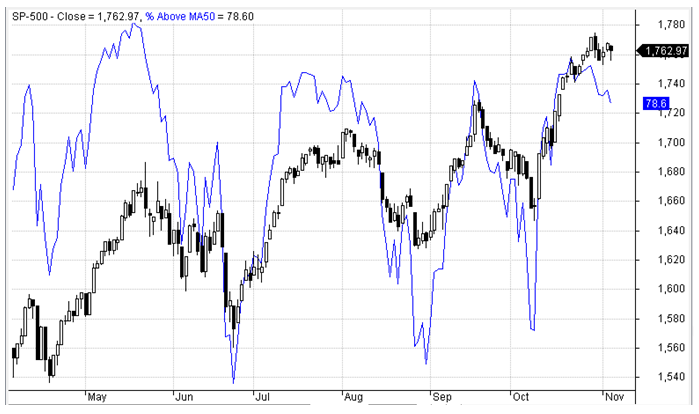

Does the percent of S&P500 stocks trading above their 50 day moving average predict future market returns? Over the last several weeks, I have seen several charts of the percent of S&P500 stocks trading above their 50 (or 200) day moving average overlaid on the S&P500. From these charts, it appears one could build a market timing indicator. The concept really looks like it has promise.

Chart from April to November 2013.