- in Mean Reversion , Research by Cesar Alvarez

How to turn a losing strategy to a winning strategy with commissions

A mean reversion strategy I trade was developed with another researcher. This strategy enters on a further intraday weakness with a limit order and typically exits a few days later when the stock bounces. Recently this researcher sent me and email saying “Try the strategy as a day trade. Enter at the open and exit at the close. Surprisingly good results.”

Of course, this piqued my interest and I went off and changed the code and ran it. The new strategy lost money. Hum. Why the difference?

Step 1: The Rules

Well, I know that we are not trading the exact same rules. Maybe there is a difference in our rules causing the big difference in results. I send him my rules. He codes them up and we are still getting very different results.

Step 2: The Trades

The next step is to check individual trades. We find a couple of minor difference because of different settings in AmiBroker and assumptions we are making. But still the difference is there.

Step 3: The Aha Moment

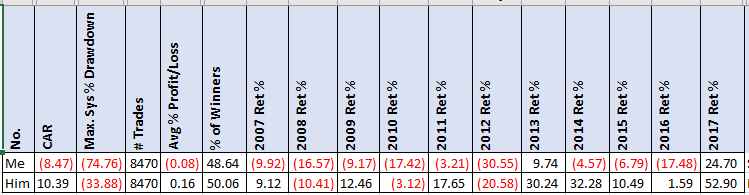

I am pounding my head on why the differences? Then it hits me, we must be using different assumptions for commissions. I go to email the researcher on this and I see I just got an email from him. He says it is the commissions causing the difference. I have been using $.01/share commissions. While he has been using InteractiveBrokers commission schedule: $.005/share with a $1 minimum and a .5% maximum of value of position. Wow, I am surprised that this could be it.

Various Commission Values

Here are the results of using various values for the commission.

Notice the last row with no commissions. A CAR of 28% compared to -8.47% with using a $.01/share. A huge difference. Your assumption on what to use for commissions would change whether you would consider trading this strategy or not.

When your edge is only .35% for an avg. % profit/loss, what you assume for the commission will have a large impact on the results. This definitely surprised me on how much the numbers changed.

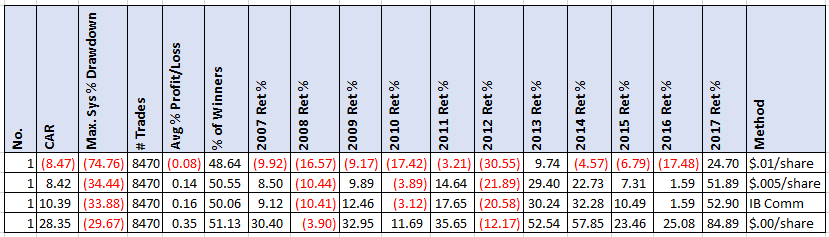

Original Strategy

How much does the original strategy change with different commission? Here are the results of the original strategy with the various commissions amounts.

I would say most of these results are about the same. Meaning one would likely trade them all or decide they are not good enough. The avg. % profit/loss here is about 4% which is much larger. Commissions are still changing the results a bit as the CAR improves by 13% when you go from $.005 to $.01 for commissions and improves 25% from $.005 to no commissions.

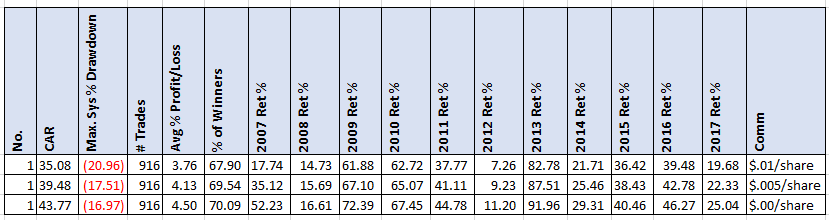

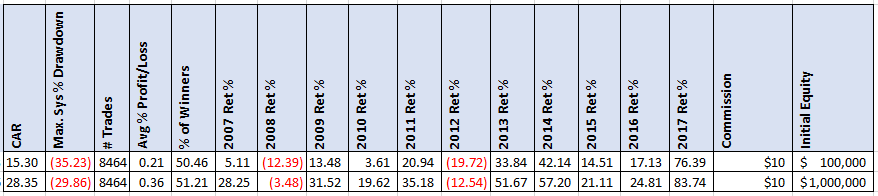

Different Starting Equity

Does starting with different amounts for the starting equity have a big impact or not?

As you can see starting with $100,000 or with $1,000,000 has no real difference. I was not expecting it to matter but it is always good to verify.

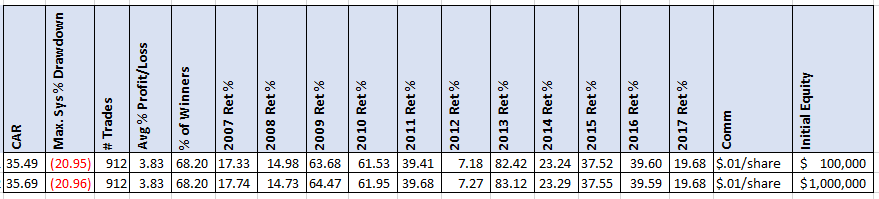

Fixed Dollar Per Trade

Some people like to use a fixed dollar amount per trade. A common value is to use $10 per trade. Now your starting equity can have a big impact. Here are the results of the day trade strategy.

Again, we see big changes in the numbers. Starting with $1 million gives nearly the same results as using $0.00/share. Personally, I do not believe that this is a good way to test unless the test time period is very short and the initial equity is the real amount you would be trading.

Final Thoughts

When you see research on the web, check the assumptions for commissions. As you can see, that assumption can have a very large impact on what you think of those results. The smaller the avg % profit/loss the larger the impact.

A recent article on Price Action Lab, Facts Vs. Fiction About Overnight Gains in SPY, also shows similar results when trading small edges and how your results change depending on your commission assumptions.

The amount we set for commissions/slippage is normally something we think about once and never go back to revisit. I have not changed the value I use in 10+ years. This was an educational exercise for me to see how big of an impact it could have in my results.

Is this a valid way to “improve” your results? It depends on how good your execution is. I don’t like to depend on it, so I will continue to use $0.01/share.

Backtesting platform used: AmiBroker. Data provider: Norgate Data (referral link)

Good quant trading,