Category Archives for "Research"

About once a month, someone asks how important it is to have dividend adjusted data. Or someone will comment they do not want to use Norgate Data because they do not adjust for dividends (it does but it is not enabled by default). My answer has been “without dividend adjusted data, your results may be understated.” It has always bothered me that I could not give a better answer. In my post, “How much does not having survivorship free data change test results?” I covered other data issues but not this one. Since Norgate Data makes it easy to have two databases, one with the dividend adjustments and one without, it was time to run tests and determine how much of a difference it makes.

In the two previous posts, we have looked at low volatility stocks vs. high volatility stocks with trailing stops. Overall, the data pointed to trading lower volatility stocks. In this post, the focus is on low volatility stocks but now adding profit target stops to see how they can improve the results.

In my last post, Should one trade high or low volatility stocks?, we placed stocks into three volatility buckets and compared their performance. Several readers pointed out that using a fixed percentage stop made it more likely for high volatility stocks to hit the stop thus not performing as well. Readers suggested using an Average True Range stop or a time stop. We will explore those two stops and see how the volatility buckets compare.

Before we get to the tests, I need to explain a new metric I will be using. At Connors Research we use Individual Trade Quality, ITQ, when we were comparing results of non-portfolio tests, such as these tests. The simple way to understand ITQ is it analogous to Sharpe Ratio in a portfolio test. To get more details on ITQ see How to Measure the Individual Trade Quality of Your Strategy.

If one is trying to develop a multi-month hold stock strategy, is it better to focus on high or low volatility stocks? For a long time, I have wanted to add a longer term stock strategy to my basket of strategies that I trade. I do not expect this strategy to perform as well as my shorter term strategies but work as a complement to them

Low volatility or high volatility? Short term trading strategies tend to do best when they focus on high volatility stocks. Will this be true for a longer hold strategy?

During some recent research I noticed that picking random stocks in the SP500 produced returns much better than I would expect. This observation was recently echoed by another researcher that I know. Could one make a market beating system by basically randomly pick stocks?

The research that led to this observation was on market timing. Can having a good market timing rule, a profit target and stop loss be enough to randomly pick stocks and beat the market. The answer may surprise you.

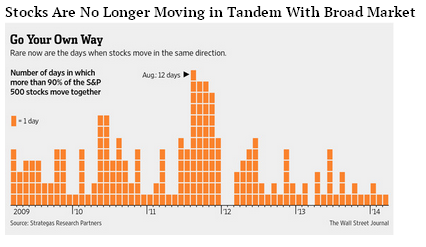

I saw this interesting graph the other day on The Big Picture and wanted to know more. Are stocks really moving less in tandem? Could there be another explanation for what is going on? Researching the numbers behind the chart may provide some interesting insights.

From: WSJ

Over the last month several people have asked me how important it is to have survivorship-free data. For any researcher this is an important question to understand how the different data can change your results. We will be exploring three potential data issues: as traded prices, delisted stocks (survivorship-bias), and historical index constituents (pre-inclusion bias).

This extended research is from two readers’ requests. Request one is adding stop losses on the “Monthly S&P500 Stock Rotation Strategy.” Request two is seeing the equity curves from “Percent S&P500 Stocks Trading Above MA50 as Market Timing Indicator.”

Is it better to buy the worst year-to-date performing stocks or the best year-to-date performing stocks for the month of December? Common wisdom would say stay away from the losers because those are the one that people are selling for tax reasons. Are fund managers buying the winners for window dressing?

My article on “Is mean-reversion dead?” produced lots of suggestions from readers on other tests to try. We will jump right in and look at what these research suggestions produced.