Category Archives for "Stocks"

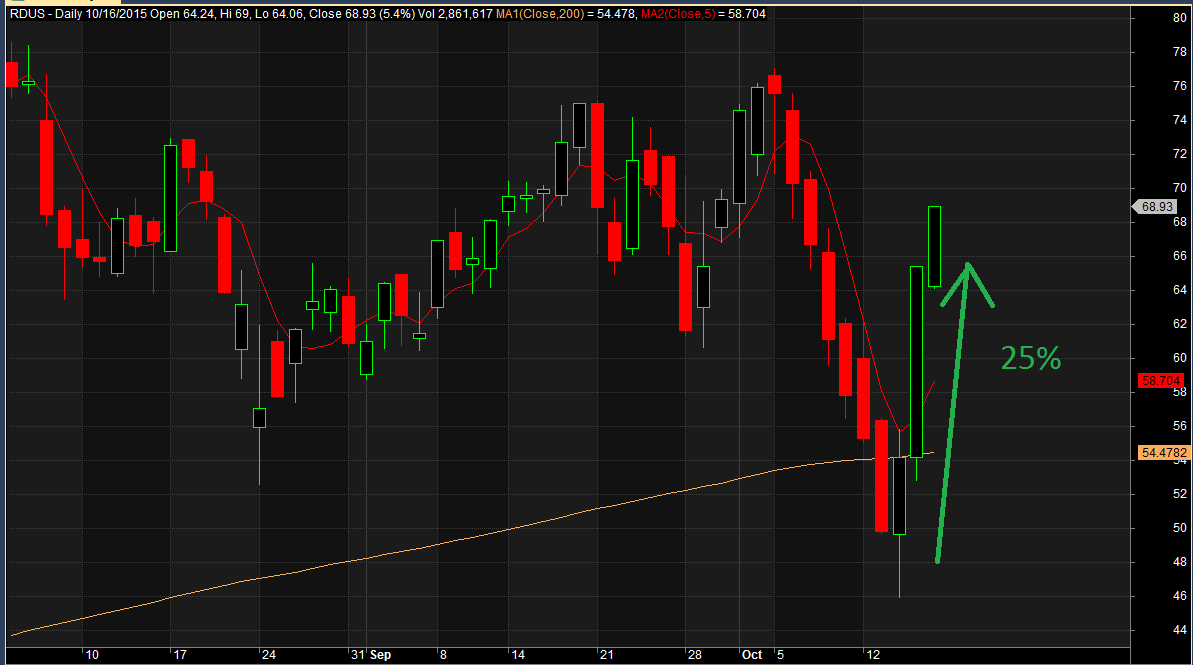

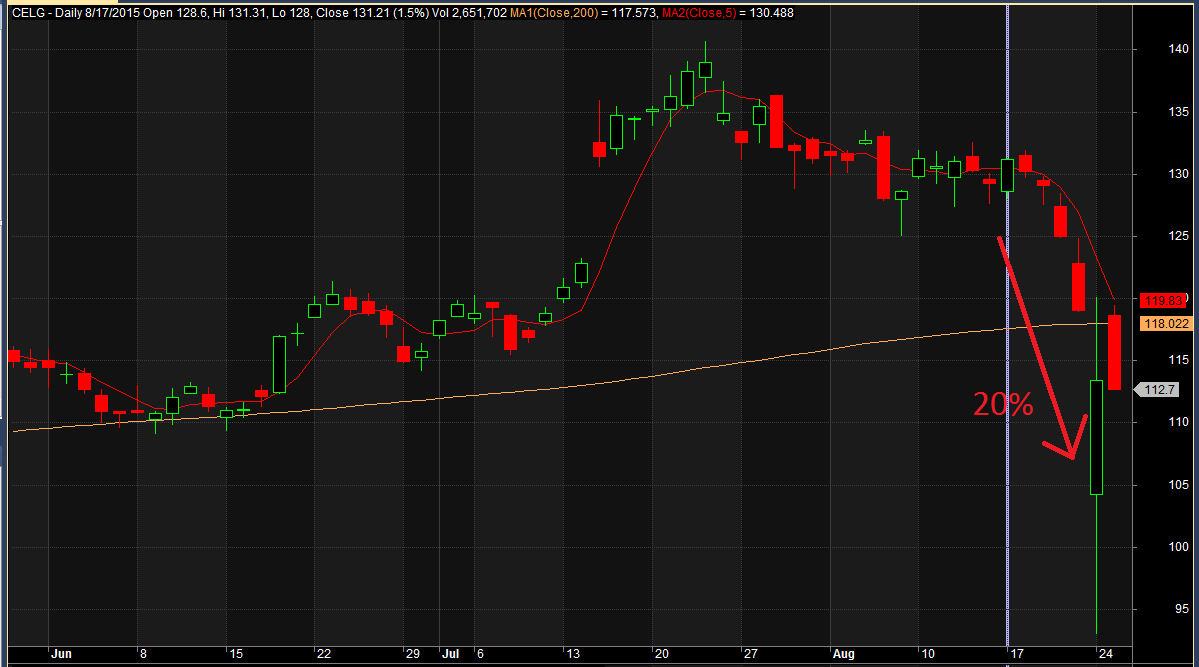

The two charts above are from recent trades I have taken. Charts created in AmiBroker.

On July 20, 2015 IBB, iShares Nasdaq Biotechnology ETF, made a closing high of 398. About three months later it closed at 289 for 27% loss. A very common thing I hear from traders is that they “don’t trade biotechnology or pharmaceutical stocks.” I completely understand. These stocks tend to be very volatile and news driven. But does removing these stocks really reduce your drawdowns? What happens to your Compounded Growth Rate? Time to see what the research shows us.

In the post, Maximum Loss Stops: Do you really need them?, we looked at how maximum loss stops changed the results of a mean reversion strategy. At the end of the post I asked the readers to vote for what to try next. Let us see how these are ideas turn out.

My previous post The Health of Stock Mean Reversion: Dead, Dying or Doing Just Fine generated good reader’s suggestions on other ways to check on mean reversion health. Let us see what these tests tell us.

My second post on this blog was a look at mean reversion, Is mean reversion dead? Given I am using a new data provider(Norgate Data), it has been almost two years since that post and there have been other articles on this recently, I figured it was time to check again. The research will focus on Russell 1000 stocks since 1995. The test is back to 1995 covers 3 bull markets and 2 bear markets.

We hear it all the time. “You must use stops.” And most of us use them. But do you know how they change your strategy results? Are they improving your results by giving you higher CAR or lower maximum drawdown? Recently I was speaking with a reader about this topic and he insisted that it you had to have stops to trade. Well, does one?

Trading stock splits is something that I have read about for long time but never researched. This article, A simple way to beat the market with stock splits, caught my eye and gave me the push to investigate the topic. This falls into the category of a topic I have heard a lot about that I can’t believe that it would work but as always one must test. One never knows.

One area of recent interest for me is trading rotational strategies on a monthly timeframe using S&P500 stocks and ETFs. Areas of exploration include Momentum and Dual Momentum. Recently I came across The Secret to Momentum is the 52-Week High??? on Alpha Architect, a blog I highly recommend on reading along with the quant mashup Quantocracy.. The article is a synopsis of research done comparing momentum vs. 52-week highs as ranking filters for a rotation strategy. A new idea I had not tried. What a great way to start the year, testing a new idea. Even though often they do not work out, one needs to be exploring all the time.

This post will cover in detail two different ways of doing Monte Carlo analysis and the code needed to it in AmiBroker. A reader recently sent me this article, Monte Carlo Analysis For Trading Systems. The article covers three methods of Monte Carlo analysis. One of which I had never thought about and I had to slap my head on how simple it was.

I recently read on Don’t Talk About your Stocks about an idea that stocks that were losers after (4, 6, 8) weeks should be sold to make way for other stocks that may do better. Will this idea improve the results from the original DTAYS Weekly Breakout Strategy? This reminded me of research I did while working for Larry Connors. On a mean reversion strategy we were researching, we noticed that after 10 days, 95% of the positions end up being losers. Then came the ‘obvious’ rule to add. Exit a position if it had not bounced after 10 days. We both thought this would greatly improve the results. It did the opposite and hurt them. Why? Because it was better to wait for the bounce even if the trade was a loser.

The Simple Ideas for a Mean Reversion Strategy with Good Results post generated lots of comments and emails about other ideas to try. This post will cover three of the most interesting ones.