March 16, 2016

- in Mean Reversion , Stocks by Cesar Alvarez

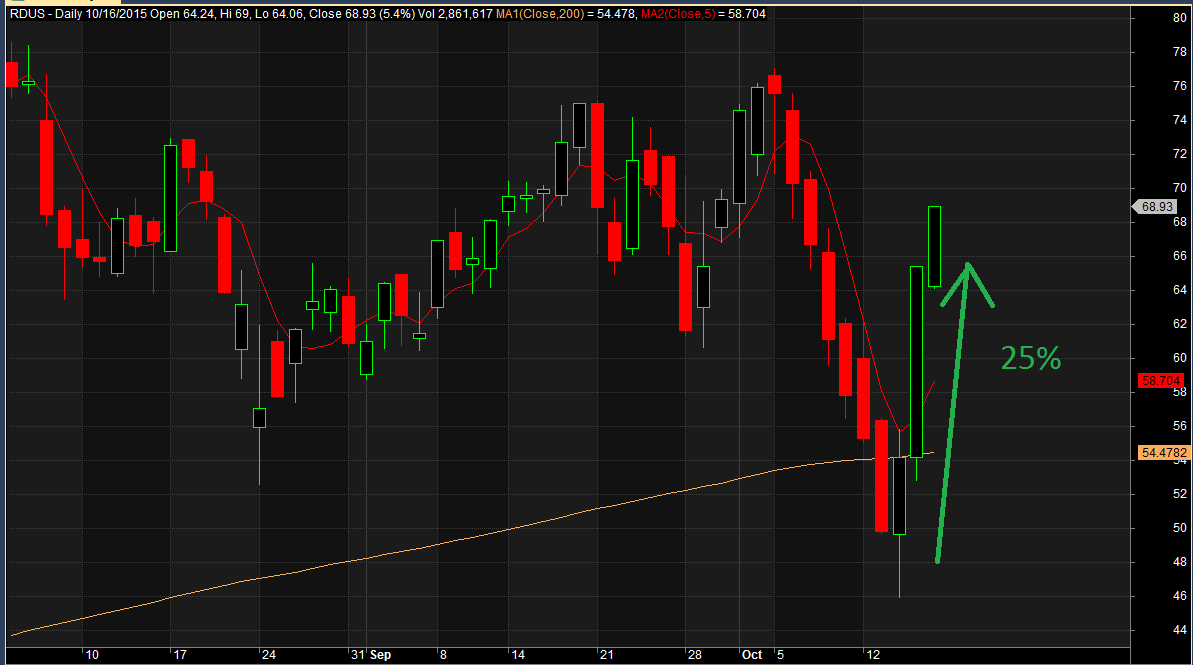

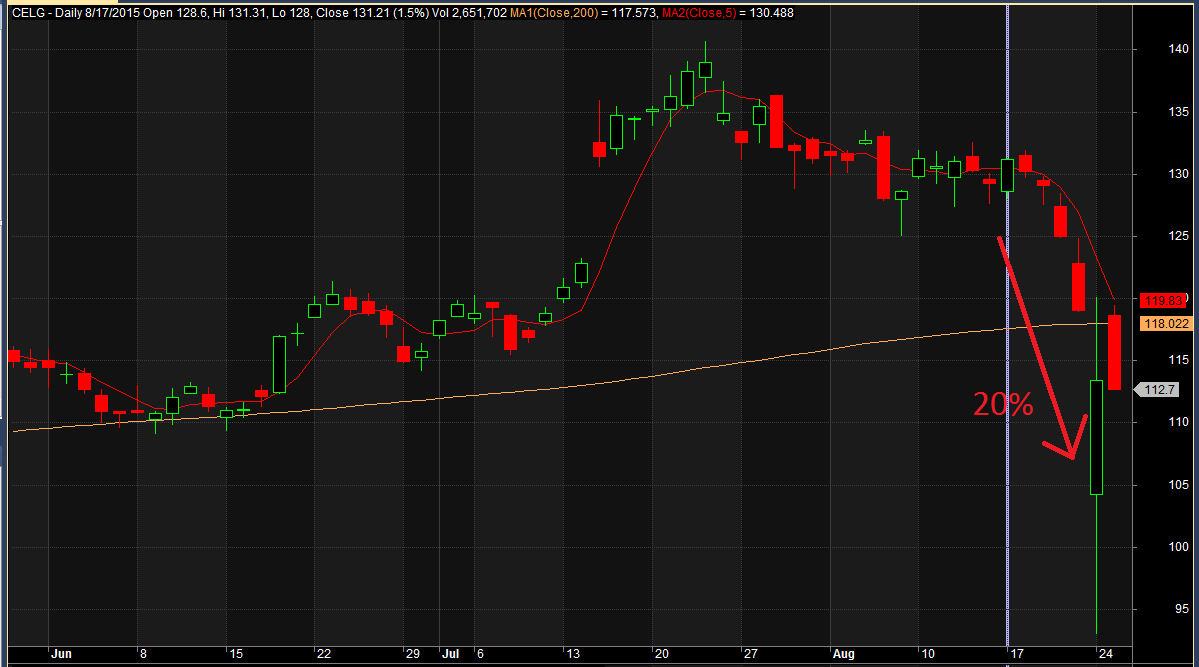

Adding Stops and Scaling Out to a Mean Reversion Strategy

I came on an idea recently that I had tested. I have tested adding max loss stops to a mean reversion strategy, with no success. See this post for more on that. About eight years ago, I tested scaling out of trades. But this person claimed that adding the two together was how to improve a mean reversion strategy. Interesting idea I had not tested.

I have a one question poll below about what to do with my research. Take 15 seconds to fill it out.